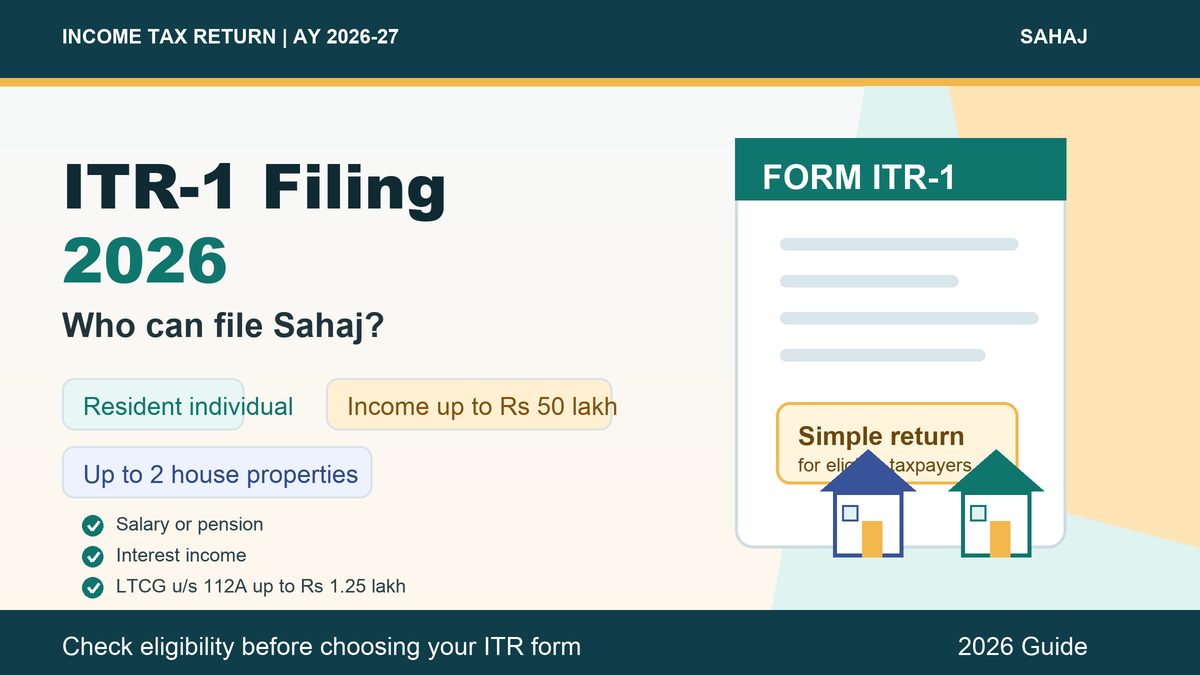

ITR-1, also known as Sahaj, is the simplest income tax return form for many salaried individuals and pensioners in India. It is mainly meant for resident individuals with simple income details and no complex sources such as business income, foreign assets or large capital gains.

For Assessment Year 2026-27, the Income Tax Department's return utility states that ITR-1 can be used by eligible resident individuals having total income up to Rs 50 lakh. A major update is that taxpayers can now report income from up to two house properties in ITR-1, subject to other eligibility conditions.

Who Can File ITR-1 for AY 2026-27?

You may file ITR-1 if you are a resident individual, other than a resident but not ordinarily resident, and your total income does not exceed Rs 50 lakh during the financial year.

ITR-1 is generally suitable if your income comes from:

- Salary or pension

- Up to two house properties

- Other sources such as savings account interest, fixed deposit interest or family pension

- Agricultural income up to Rs 5,000

- Long-term capital gains under Section 112A up to Rs 1.25 lakh

- Clubbed income of spouse or minor child, if the income falls under the permitted categories

This makes ITR-1 useful for salaried taxpayers, pensioners and individuals with limited interest income or simple house property income.

What Is the Rs 50 Lakh Income Limit?

The basic income limit for ITR-1 is Rs 50 lakh. If your total income is more than this limit, you should not use ITR-1. In such cases, ITR-2 or another applicable return form may be required, depending on your income sources.

Taxpayers should also check Form 16, AIS, Form 26AS, bank interest certificates and capital gain statements before choosing the return form.

Two House Property Rule in ITR-1

For AY 2026-27, ITR-1 allows reporting income from up to two house properties. This is helpful for taxpayers who, for example, live in one house and earn rent from another, or own two rented residential properties.

However, this relaxation is limited. If you have income from three or more house properties, ITR-1 is not the correct form. You may need to use ITR-2, provided you do not have business or professional income.

Who Cannot File ITR-1?

You should not file ITR-1 if any of the following applies to you:

- You are a non-resident or resident but not ordinarily resident

- Your total income is above Rs 50 lakh

- You have income from business or profession

- You have income from more than two house properties

- You have short-term capital gains

- Your LTCG under Section 112A exceeds Rs 1.25 lakh

- You are a director in a company

- You held unlisted equity shares during the year

- You have foreign assets, foreign income or signing authority in a foreign account

- You have brought-forward losses or losses to be carried forward

- Tax was deducted under Section 194N

- Tax on ESOPs has been deferred

Choosing the wrong ITR form can lead to defective return notices, so it is better to confirm eligibility before filing.

New Tax Regime and Form 10-IEA

For individuals filing ITR-1 or ITR-2 without business income, a separate Form 10-IEA is generally not required for selecting the tax regime. The option can be chosen directly in the ITR form.

Form 10-IEA mainly becomes relevant for individuals or HUFs having business or professional income. Since ITR-1 is not meant for business income, most ITR-1 filers only need to select the applicable tax regime inside the return.

Is Employment Type Mandatory?

Yes. While filing ITR-1, taxpayers must choose the correct nature of employment, such as central government employee, state government employee, PSU employee, pensioner, private sector employee or not applicable.

This helps the tax department classify salary and pension details correctly.

Final Words

ITR-1 is designed for simple tax returns, but taxpayers should not assume they are eligible just because they are salaried. Check your income limit, capital gains, house property details, foreign asset status and losses before filing.

For AY 2026-27, the biggest relief is the ability to report income from up to two house properties in ITR-1. Still, if your income profile is complex, it is safer to use the correct ITR form or consult a tax expert.

Disclaimer: This article is for general information only and should not be treated as tax or legal advice.