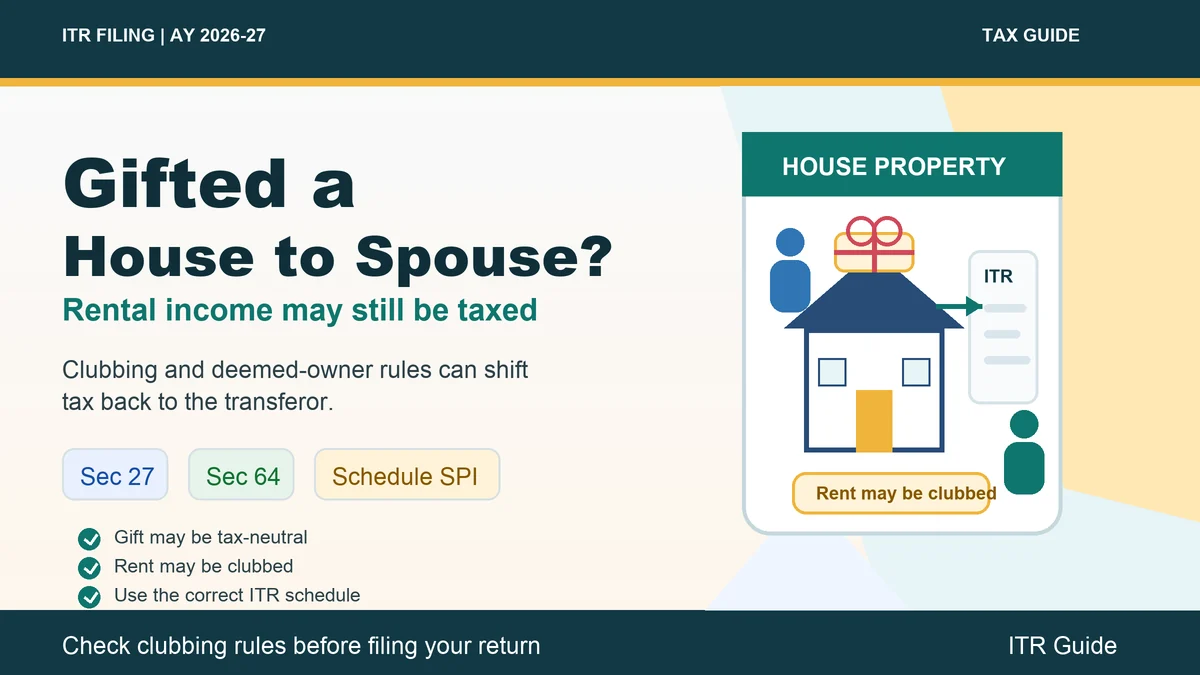

Many taxpayers transfer a house property to their spouse for family planning, convenience or estate reasons. After the gift, the property may legally stand in the spouse's name, and the spouse may even receive rent from tenants.

But income tax rules do not always follow only legal ownership. In some cases, the person who gifted the property may still be treated as the owner for tax purposes.

This is where Sections 27 and 64 of the Income-tax Act become important.

Key Takeaways

- Gifting a house to a spouse may not create immediate income tax on the gift, but rent may still be taxable in the transferor's hands.

- Section 27 can treat the person gifting the house as the deemed owner for house property income.

- Section 64 may club income from assets transferred to a spouse without adequate consideration.

- Gifting money to your spouse to buy a house may also attract clubbing rules.

- Report such income correctly in the applicable ITR form to avoid mismatch or tax notices.

The Gift May Be Tax-Neutral

A gift from one spouse to another is generally not taxed as income in the hands of the receiving spouse because spouse is treated as a relative under gift taxation rules.

However, stamp duty, registration cost and state-level charges may still apply depending on the location of the property.

Rental Income May Not Shift Automatically

If you gift a house to your spouse without adequate consideration, you cannot assume that future rent will be taxed only in your spouse's return.

For income tax purposes, the rent may still be linked back to the person who transferred the property.

Section 27 Creates Deemed Ownership

Section 27 can treat the transferor spouse as the deemed owner of a house property if it is transferred to the spouse without adequate consideration.

This means that even if the property papers show your spouse as owner, the rental income may still be taxable in your hands.

Section 64 Also Supports Clubbing

Section 64 deals with clubbing of income. If an individual transfers an asset to a spouse without adequate consideration, income arising from that asset can be included in the income of the person who made the transfer.

So, if rent is earned from a gifted property, the tax department may ask the transferor to include that rent in their own ITR.

Gifting Money May Also Attract Clubbing

Some taxpayers gift money instead of gifting the house directly. If your spouse uses that gifted money to buy a house, rental income from that house may still be clubbed with your income.

The tax impact may depend on the source of funds and how much each spouse contributed.

There Are Exceptions

The clubbing and deemed ownership rules may not apply in every case. For example, where the transfer is made under an agreement to live apart, different treatment may apply.

Transfers made for adequate consideration may also be treated differently.

Report Correctly in ITR

If rent is taxable in your hands due to clubbing or deemed ownership, report it properly in the applicable ITR form. Do not ignore the income just because rent is credited to your spouse's bank account.

Where required, use the clubbed-income or specified-person reporting section in the applicable ITR form.

Final Words

Gifting a house to your spouse may look simple, but the tax treatment of rental income can be tricky. Legal ownership and tax ownership may not always be the same.

Before filing ITR for AY 2026-27, check whether Sections 27 and 64 apply to your case. If the property earns rent, it is better to confirm reporting with a tax professional instead of assuming the income belongs only to the spouse.

Disclaimer: This article is for general information only and is not tax advice. Please consult a qualified tax professional for your specific case.